ISLAMIC ETHOS

Principles before profits · Conviction before convenience

From our fund creation process to our day-to-day operations, Qibla Capital is built on a foundation of Islamic principles. These principles are not a marketing pitch: they are the first and most important filter we apply in evaluating every decision. Every step begins with and is governed by the question: Is this truly and fully Halal-compliant?

Our principal anchor is the Qur’anic ethic of we hear and we obey (samiʿna wa aṭaʿna / سَمِعْنَا وَأَطَعْنَا). When Allah issues an explicit command, it is incumbent on us to submit to His Majesty with humility and faithful obedience.

Our Conviction

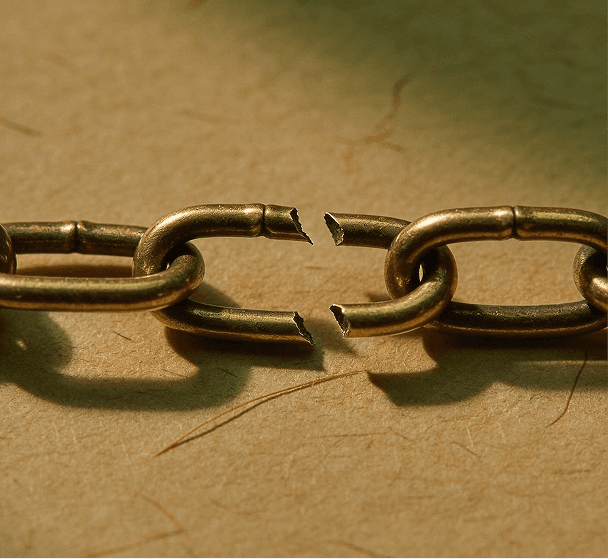

The Impermissibility of Riba

Riba (interest / usury) is among the most explicitly and emphatically prohibited acts in Islam. In Surat Al Baqarah, Allah issues a stark warning to those who persist in interest-based dealings:

"O believers! Fear Allah, and give up outstanding interest if you are true believers. If you do not, then beware of a war with Allah and His Messenger! But if you repent, you may retain your principal, neither inflicting nor suffering harm."

QUR'AN 2:278—279

This verse leaves little room for interpretive flexibility. Riba is categorically haram and cannot be made permissible through any form of creative structuring. Consequently, any financial instrument that is derived from, or dependent upon, interest is, in our view, intrinsically impermissible.

"Easing Hardship"

raf' al-haraj / رفع الحرج

Beginning in the late 1990s, several Islamic finance bodies developed criteria to allow investments in companies that engage in riba. According to AAOIFI, investment in stocks is permissible if the company's primary business is halal and the company meets the below financial ratios:

- —Interest-bearing debt and deposits do not exceed 30% of market capitalization, and

- —Income from haram activities does not exceed 5%.

This opinion is rooted in the principle of easing hardship (raf' al-haraj / رفع الحرج) and has been adopted by many modern "halal" financial products and services.

We, respectfully, do not hold this opinion.

Hardship (haraj) in Islamic fiqh refers to situations of genuine necessity, such as starvation, death, or great harm. In these instances, prohibited acts may be temporarily permitted to prevent greater harm.

Accordingly, we do not view a lack of accessible investment options as a hardship. Choosing to refrain from participating in riba-based investments, even at the cost of sitting on cash and paying Zakat on the idle capital, is not hardship nor a necessity; it is principled obedience and disciplined restraint.

We believe that doing what is right is not always easy, but ease is not the determining measure of halal and haram.

The "One-Third" Hadith

Declaring that interest is permissible below a numerical threshold is, in our view, analogous to claiming that pork becomes halal when consumed in small quantities.

The threshold numbers extrapolated by AAOIFI for interest-bearing debt are drawn by analogy from the hadith of Sa'd ibn Abi Waqqas.

HADITH

Sa'd said: "I was stricken by an ailment that led me to the verge of death. The Prophet (S) came to pay me a visit. I said, 'O Allah's Apostle! I have much property and no heir except my single daughter. Shall I give two-thirds of my property in charity?' He said, 'No.' I said, 'Half of it?' He said, 'No.' I said, 'One-third of it?' He said, 'You may do so, though one-third is also excessive.'"

Sahih al-Bukhari, Book of Wills, Hadith 2735

This hadith is specifically related to moderation in voluntary charitable bequests at the end of one's life in order to protect the rights of heirs. We, humbly, are not comfortable with invoking a Hadith that regulates restraint in a permissible and virtuous act (charity) to justify and rationalize participation in a Quranically forbidden and morally blameworthy act (riba).

The 5% Haram Income Rule

Under the AAOIFI standards adopted by many modern "halal screening" frameworks, companies are permitted to derive up to five percent (5%) of their revenue from haram sources on the basis that such income is deemed "immaterial."

Qibla Capital unequivocally rejects this premise.

In Islamic law, a ruling follows the nature of an action or income, not its proportion. Whatever Allah has declared haram does not become halal by dilution.

At its core, the rule is arbitrary and not drawn from the Qur'an or Sunnah, nor from any established principle of Islamic jurisprudence. Rather, it is borrowed from conventional accounting concepts of "materiality," as used in IFRS reporting and common financial disclosure practices. A haram amount that may be immaterial for accounting purposes remains fully haram and fully material for Islamic legal purposes.

Islamic Principles

Our Halal filters include, but are not limited to

No Haram Industries

No alcohol, cannabis, predatory finance, gambling, pork, weapons manufacturing, etc.

No Interest-Based Debt

No interest-based debt or interest income (zero tolerance)

No Gharar

No gharar (excessive uncertainty in contracts)

Permissible Sources

No income from impermissible sources

Transparent Ownership

Transparent ownership structures

Ethical Treatment

Ethical treatment of employees and customers

Mudārabah

مضاربةOur business model follows the Islamic concept of "trustee finance", or Mudārabah / مضاربة.

This passive partnership is one where one party provides the capital (Rabb al Māl /رب المال) and the other provides labor (Muḍārib / مضارب) while both share in the profits.

Risk Structure

In the event of loss, it is fully borne by the Rabb al Māl unless the loss results from misconduct, negligence, or breach of contract by the Muḍārib.

Our Model

Qibla Capital serves as the Muḍārib, managing acquisitions and operations, while investors serve as the Rabb al Māl. Both parties share in the profits.

Prophet Muhammad's wife Khadija used a Mudaraba contract with Prophet Muhammad in his trading expeditions throughout northern Arabia, with Sayyida Khadija providing the capital and Prophet Muhammad (S) providing the labor / entrepreneurship.

Halal Oversight Board

Qibla Capital operates under a robust halal governance framework rooted in accountability and transparency.

An independent Halal Oversight Board composed of Islamic scholars will review every deal, structure, and transaction. The role is independent and their oversight is meant to hold us to the highest standards of Islamic finance.

This oversight helps us maintain:

- Integrity in decision-making

- Transparency in structures

- Accountability to stakeholders

Halal Governance & Accountability

To uphold the highest Islamic standards, the HOB is granted full visibility into Qibla Capital's operations, investments, and structures and reviews all matters at three critical stages:

Corporate structure & setup:

The HOB reviews the QC governing documents, corporate policies, capital structure, subsidiary ownership arrangements, and governance mechanisms to ensure alignment with Islamic finance principles.

Pre-acquisition & transactional diligence:

QC seeks initial halal clearance before advancing beyond preliminary discussions, and each potential acquisition is screened for halal compliance prior to commitment. Reviews cover revenue streams, operational practices, governance structures, contracts, and financing arrangements to identify and mitigate any compliance risks.

Ongoing operational monitoring:

Subsidiaries undergo annual compliance reviews covering financials, revenue composition, business activities, contracts, and financing arrangements. Any material changes that could affect compliance are assessed promptly, with corrective measures implemented where necessary.

The Structural Problem with

Modern "Halal" Screening

None of the commonly used "halal screening" methodologies today offers an outright rejection of haram revenue or interest-based debt. As the global finance system is deeply intertwined in interest-based finance, trying to "screen" such a system inevitably leads to compromise rather than compliance. This explains exactly why Qibla Capital exists: to build a parallel Islamic financial ecosystem where principles come first and profits come second.

These methodologies have an initial filter where they screen out companies whose core business is primarily haram, such as alcohol, gambling, insurance, weapons, etc.

After, the focus shifts almost entirely to financial ratios. However, many overlook ethics as a core part of halal and haram. A company may pass a halal screen because its numbers fall within acceptable limits, yet still be involved in serious ethical harms, creating moral, reputational, and long-term business risk for investors.

COMPARISON OF SHARIAH STANDARDS

AAOIFI

- Haram Revenue

- <5%

- Total Debt

- /Market Cap <30%

- Cash + Interest

- /Market Cap <30%

- A/R + Cash

- —

MSCI Index Series

- Haram Revenue

- <5%

- Total Debt

- /Total Assets <30%

- Cash + Interest

- <30%

- A/R + Cash

- <30%

MSCI Index M- Series

- Haram Revenue

- <5%

- Total Debt

- /Avg. 36 mo. Market Cap <30%

- Cash + Interest

- <30%

- A/R + Cash

- <46%

FTSE

- Haram Revenue

- <5%

- Total Debt

- /Total Assets <33.33%

- Cash + Interest

- <33.33%

- A/R + Cash

- <50%

S&P

- Haram Revenue

- <5%

- Total Debt

- /Trail. 24 mo. Market Cap <33%

- Cash + Interest

- /Trail. 24 mo. Market Cap <33%

- A/R + Cash

- /Trail. 1 mo. Market Cap <33%

ISRA

- Haram Revenue

- <5%

- Total Debt

- /Avg. 24 mo. Market Cap <33%

- Cash + Interest

- <33%

- A/R + Cash

- —

SAC

- Haram Revenue

- —

- Total Debt

- /Total Assets <33%

- Cash + Interest

- —

- A/R + Cash

- —

STANDARD

REVENUE

BEARING SECURITIES

| AAOIFI | <5% | /Market Cap <30% | /Market Cap <30% | — |

| MSCI Index Series | <5% | /Total Assets <30% | <30% | <30% |

| MSCI Index M- Series | <5% | /Avg. 36 mo. Market Cap <30% | <30% | <46% |

| FTSE | <5% | /Total Assets <33.33% | <33.33% | <50% |

| S&P | <5% | /Trail. 24 mo. Market Cap <33% | /Trail. 24 mo. Market Cap <33% | /Trail. 1 mo. Market Cap <33% |

| ISRA | <5% | /Avg. 24 mo. Market Cap <33% | <33% | — |

| SAC | — | /Total Assets <33% | — | — |

Qibla Capital operates under a strict no-compromise policy with respect to interest, haram income, and unethical industries. We do not permit intentional exposure to haram instruments, regardless of percentage threshold, hardship argument, or market convention.

Any non-compliant income that arises inadvertently is fully segregated and donated to charity without benefit to the Company or its investors.

Ready to invest with us?

We would be honored to have you as our partner on this journey.

Contact Us

If you are selling your business, referring a business for sale, or interested in joining our internship program, please email us at[email protected]or use the form below.